HVAC finance options for energy-efficient upgrades

TL;DR:

- Most UK homeowners and businesses need to combine public grants with private loans to fund energy-efficient HVAC upgrades due to market fragmentation.

- Eligibility varies by scheme, technology, and location, with grants like the BUS significantly reducing upfront costs.

Most homeowners and business owners assume there is one clear, government-backed route to funding an energy-efficient HVAC upgrade in the UK. There is not. The reality is that green HVAC financing is fragmented, meaning no single universal scheme covers every technology, every household, or every region. Instead, the most effective approach almost always involves combining public grant support with private borrowing. This guide cuts through that confusion, walking you through the key public schemes, your private finance options, and how to pair them intelligently so your upgrade is both affordable and stress-free.

Table of Contents

- How UK HVAC finance really works: The fragmented landscape explained

- Public grant support: Who is eligible and what schemes exist?

- Private sector finance: Loans, green mortgages and flexible repayments

- Pairing grants with finance: A practical walkthrough

- The hidden pitfalls and what most guides miss about HVAC finance

- Upgrade your HVAC system with flexible, expert-backed solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| No universal scheme | UK HVAC financing is fragmented, so most homeowners must mix grants with private finance options. |

| Grant eligibility matters | Schemes like BUS offer up to £7,500 off but have tight eligibility rules—location and heat pump type are critical. |

| Loans fill the gap | After grants, private lenders provide loans or green mortgages, often requiring credit checks and flexible repayment structures. |

| Hybrid systems excluded | Hybrid heat pump systems are not supported by BUS, so check technical eligibility before planning finance. |

| Double-check before signing | Always confirm grant approval and loan terms with both providers before committing to any installation. |

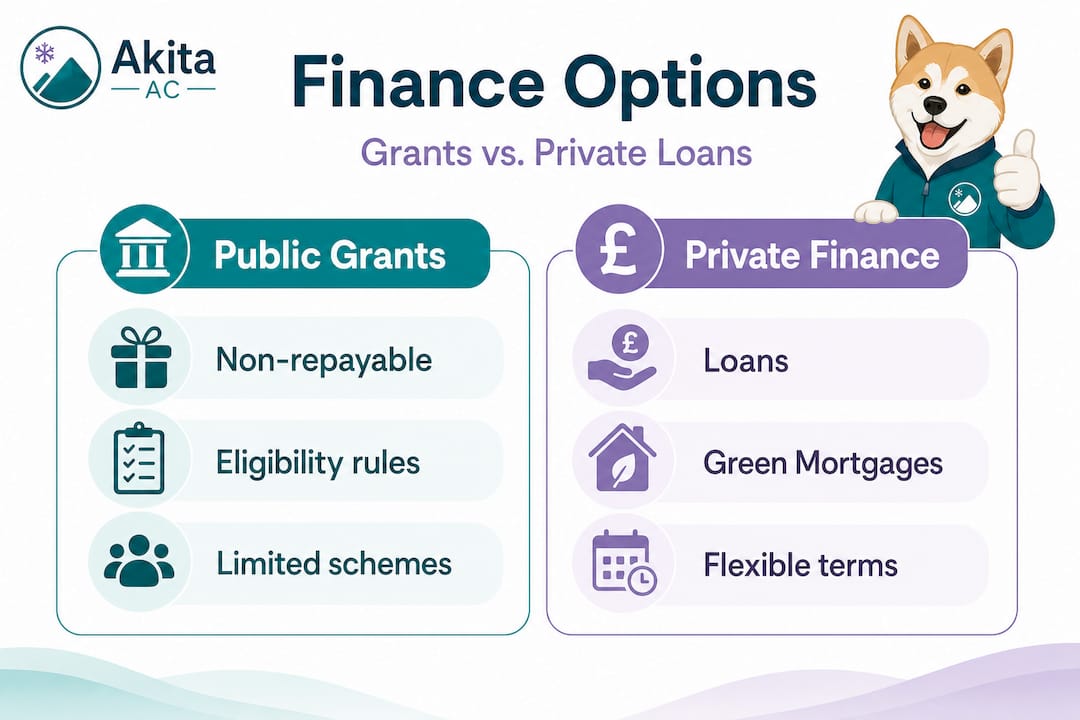

How UK HVAC finance really works: The fragmented landscape explained

If you have spent any time researching HVAC finance in the UK, you have probably noticed that the answers depend heavily on where you live, what system you want to install, and whether you own your property outright. There is no single portal, no one application form, and no universal eligibility criteria. Understanding this upfront saves enormous frustration.

The UK market operates on a patchwork model. Public grants funded by central government are non-repayable, meaning you do not pay them back, but they come with specific eligibility restrictions. Private finance products such as unsecured loans, green mortgages, and vendor finance are repayable and subject to credit assessment. Financing air conditioning or heat pump installations for most households therefore means working across both worlds simultaneously.

Here is a simplified overview of how the two pillars of UK HVAC finance compare:

| Feature | Public grants (e.g., BUS) | Private finance (loans, green mortgages) |

|---|---|---|

| Repayable? | No | Yes |

| Requires credit check? | No | Yes |

| Geographic limits? | England and Wales only (BUS) | UK-wide, lender dependent |

| Technology restrictions? | Yes (e.g., no hybrid systems) | Varies by lender |

| Typical value | Up to £7,500 | Variable, up to full cost |

| Application route | Via MCS-certified installer | Direct to lender or vendor |

“The fragmented nature of the UK market means most households end up stacking public support with private borrowing or green-mortgage features to cover total installation costs.” This is the reality for the majority of people upgrading their HVAC in UK homes today.

Research into consumer attitudes confirms that demand for retrofit finance is particularly strong when low or zero-interest terms are on offer alongside awareness of grants like the Boiler Upgrade Scheme. In other words, affordability mechanics really do shape whether people act. Understanding the landscape is not just theoretical; it determines whether your upgrade happens this year or gets pushed back indefinitely.

The key insight here: treat public grants as the first tool you reach for, then layer private finance on top for any remaining balance. This sequencing matters, and we will walk through it step by step later in this guide.

Public grant support: Who is eligible and what schemes exist?

The most significant public mechanism currently available for HVAC and heat pump upgrades in England and Wales is the Boiler Upgrade Scheme, commonly known as BUS. It provides non-repayable grants paid directly to your MCS-certified installer, reducing your upfront cost rather than arriving as a cheque in your bank account. Knowing exactly what is covered and who qualifies is essential before you plan your budget.

For most UK homeowners, the BUS grant is the most direct way to reduce the upfront cost of a heat pump installation. Here are the current grant levels:

| Technology | BUS grant amount |

|---|---|

| Air source heat pump | Up to £7,500 |

| Ground source heat pump | Up to £7,500 |

| Biomass boiler | Up to £5,000 |

These are meaningful sums. On an air source heat pump installation that might cost between £10,000 and £15,000 in total, a £7,500 BUS grant takes a large chunk off the top before you even consider financing the rest. That materially changes the scale of private borrowing you need.

Key eligibility points you need to know:

- Property type: You must own your home or a small commercial property. Renters cannot apply directly.

- Location: The BUS is available in England and Wales only. It does not apply in Scotland or Northern Ireland, where separate schemes operate.

- Installer requirement: Your installer must hold MCS (Microgeneration Certification Scheme) certification. Non-certified installers cannot access or apply for the grant on your behalf.

- Existing heating system: You must currently use fossil-fuel heating. Some exceptions apply for properties moving away from electric storage heaters.

One critical exclusion that catches many buyers off guard: hybrid heat pump systems that retain a fossil-fuel boiler as backup are not supported under BUS. If your plan involves keeping your existing gas boiler running alongside a new heat pump, you will not qualify. This is an important distinction when evaluating which system suits your property and budget.

The range of types of air conditioning systems eligible for grant support is narrower than many assume, which makes early-stage planning with a qualified installer genuinely valuable rather than just a sales call.

Pro Tip: Always verify your installer’s MCS certification on the official MCS register before signing any contracts. Without this, no BUS grant can be claimed, regardless of how well the installation goes.

Scheme rules are also subject to change. The BUS has been extended and adjusted several times since its launch, and grant amounts may shift with future government budget decisions. Checking current eligibility criteria directly with the Energy Saving Trust or your installer before committing to a specific technology is sensible practice.

Private sector finance: Loans, green mortgages and flexible repayments

Even with a grant in hand, many homeowners and businesses still face a remaining balance of several thousand pounds. That is where private finance options become important. The good news is that the market for green lending has grown considerably, and several products are specifically designed to support energy-efficient upgrades.

Your main options once you have explored grant eligibility:

- Unsecured personal loan. Available from high street banks, credit unions, and specialist green lenders. Interest rates vary significantly depending on your credit profile. You borrow a fixed sum and repay over an agreed term, typically two to ten years.

- Green mortgage or further advance. Some mortgage lenders offer discounted rates or additional borrowing specifically for energy-efficient home improvements. If your home’s Energy Performance Certificate (EPC) rating improves after installation, you may qualify for better terms on remortgage.

- Vendor or installer finance. Many HVAC installers, including those working within the Akita network, offer their own finance arrangements, sometimes at promotional zero-interest rates for qualifying customers. This can be the most straightforward route for smaller balances.

- Government loan schemes. The UK’s Warm Homes Plan includes both grant and loan options for heat pumps, potentially widening access for households who do not qualify for grant funding outright.

Consumer demand for retrofit finance is strongest where zero-percent interest rates and flexible repayment structures are available. If you are comparing finance products, prioritise these two factors above headline loan amounts. A slightly larger loan at zero percent over five years is almost always better value than a smaller loan at eight percent over two years.

It is equally important to understand that private finance is not automatic. Lenders apply affordability and credit checks, and eligibility for a public grant does not guarantee you will also qualify for a preferential loan rate. These are two separate processes. Some households find they qualify for grant support but struggle with lender affordability criteria; others have excellent credit but do not meet geographic or technology eligibility for grants. Planning for both assessments simultaneously avoids unpleasant surprises mid-project.

Pro Tip: When comparing loan offers, always ask for the total cost of credit, not just the monthly repayment. Two products with identical monthly costs can have very different total repayment figures depending on the term length.

Choosing an energy-efficient HVAC system early in the process also helps, because some finance products are tied to specific technology ratings or installer certifications. Knowing your system specification before approaching lenders gives you a cleaner, faster application experience.

Pairing grants with finance: A practical walkthrough

Let us put this into practice with a realistic scenario. You are a homeowner in Norfolk, currently using a gas boiler, and you want to install an air source heat pump. The total installation quote is £13,000.

Here is how a combined grant and finance approach works in practice:

- Check grant eligibility first. You are in England, you own your home, and your installer holds MCS certification. You qualify for the BUS. The grant reduces your costs by up to £7,500, leaving a balance of £5,500.

- Your installer applies for the grant. The BUS application is made by your MCS-certified installer, not by you directly. The grant is paid to them and deducted from your invoice. You never handle the grant money yourself.

- Assess your remaining finance need. With the £7,500 grant applied, you need to fund £5,500. This is a much more manageable borrowing amount than the full £13,000.

- Compare finance products for the balance. Contact your bank, check green mortgage options, and ask your installer about any zero-interest vendor finance. Get written offers before making any final commitments.

- Apply for finance and get written confirmation. Do not assume verbal approval is sufficient. You need written confirmation from both the grant scheme (via your installer) and your finance provider before authorising installation to begin.

- Proceed with installation. Once both pieces of the funding puzzle are confirmed in writing, you can schedule your installation with confidence.

Getting written confirmation from both the grant scheme and your lender before work begins is not bureaucratic caution. It is the step that protects you if anything changes at the last minute.

Common pitfalls to avoid at each stage: do not choose a hybrid system expecting grant support (it will not come), do not begin installation before finance is confirmed, and do not assume your postcode is eligible without checking. These three mistakes account for the majority of frustrating experiences in the HVAC upgrade process.

Upgrading your home HVAC does not need to be high-risk financially. When you sequence the process correctly, the combination of grant and finance is a genuinely powerful tool for making modern, efficient systems accessible.

The hidden pitfalls and what most guides miss about HVAC finance

Here is something that most finance guides will not tell you plainly: the landscape changes. Grant schemes are extended, adjusted, capped, and occasionally withdrawn with relatively short notice. What works in 2026 may not be available in the same form next year, and what is unavailable now might return with a different structure under a different programme name.

We have seen clients lose grant eligibility because they waited too long after receiving an initial quote. In that time, installer certifications expired, scheme rules were updated, or property eligibility criteria shifted. The lesson is not to panic, but to act within a reasonable timeframe once you have confirmed your position.

The other thing most guides gloss over: your final finance offer depends entirely on a lender’s assessment of you at the time of application. Scheme eligibility does not guarantee affordable credit. We have worked with households who assumed that because they qualified for BUS, everything else would fall into place automatically. It does not always work that way. A dip in credit score, a change in employment status, or a property valuation that comes in lower than expected can all affect the private finance portion of your plan.

Certain HVAC system types are also repeatedly excluded from public schemes in ways that catch buyers off guard. Hybrid systems, as mentioned, are a classic example. But some ducted systems and commercial-grade installations can also fall outside standard grant definitions. Always get a clear written confirmation from your installer about which scheme covers which component of your installation.

The most robust approach is to treat your grant eligibility confirmation and your finance offer as two separate milestones. Do not advance past either one without written documentation. This is not overcaution; it is simply how professionally managed upgrades avoid costly surprises.

Upgrade your HVAC system with flexible, expert-backed solutions

Understanding the finance landscape is one thing; finding the right team to guide you through it is another. At Akita Air Conditioning, we work with homeowners and businesses across England and Wales to make energy-efficient upgrades genuinely straightforward.

Whether you are exploring domestic air conditioning installation for your home or need a specialist assessment for a commercial air conditioning installation, our team handles the technical and financial complexity alongside you. We serve clients throughout Suffolk, Norfolk, Essex, and the wider East Anglia region, with transparent pricing, flexible finance options, and installations carried out by certified engineers. Get in touch today to request a survey or discuss your upgrade options with someone who knows the local market and the grant landscape well.

Frequently asked questions

Who can apply for the Boiler Upgrade Scheme in the UK?

Homeowners and small business property owners in England and Wales are eligible; the scheme is not available in Scotland or Northern Ireland.

Is it possible to combine a public grant with a loan for my HVAC upgrade?

Yes, most UK households combine a grant such as BUS with private finance to cover remaining installation costs. The key mechanism is applying the non-repayable grant first, then borrowing only what remains.

What heat pump systems are not covered by the BUS grant?

Hybrid heat pump systems that retain a fossil-fuel boiler for backup heating are explicitly excluded from BUS grant support.

What are the main requirements for private sector HVAC finance?

Most lenders require credit and affordability checks, and each product has its own eligibility criteria. Lender affordability assessments are separate from grant eligibility, so qualifying for one does not guarantee the other.

Are there any new government schemes for heat pumps apart from grants?

Yes, the UK Warm Homes Plan includes both grants and loans to support heat pump installations, potentially widening access for households who do not qualify for grant funding alone.